Goodwin: Top UK Engineer Worth Premium Shares

Looking for evidence that British manufacturing remains vibrant? Visit an understated area in Stoke-on-Trent. There, on a site occupied since the Victorian era, you’ll find Goodwin, a heavy engineering firm that ranks among the nation’s most profitable specialist manufacturers.

While it may lack glamour, Goodwin fabricates essential components that sustain vital national infrastructure. This includes precision-cast containers for nuclear waste at Sellafield, high-integrity components for naval propulsion systems, and specialized valves for the liquefied natural gas sector. These are critical elements where failure is not an option, and Goodwin’s superior expertise in producing them drives its impressive profitability. After a strong performance run, the question arises: do the shares still represent good value for investors?

Goodwin maintains strong family leadership

Established in 1883 by Ralph Goodwin, the company has stayed under family control, setting it apart from many competitors. Today, a Goodwin chairs the board, Goodwins manage operations, and the family holds majority ownership.

This structure, which might typically spark governance concerns, has proven to be Goodwin’s biggest asset. Family ownership enables patient, long-term investments without the pressure for short-term gains. The focus has been on securing contracts emphasizing quality and reliability over cost-cutting. This approach has earned the company deep respect within the industry, building a reputation over decades that newcomers struggle to match.

A distinctive feature is Goodwin’s proactive strategy to adapt to change rather than resist it. A decade ago, the firm appeared heavily dependent on oil and gas. When prices plummeted, it chose reinvention over contraction, aggressively entering high-barrier sectors like defence, nuclear power, and other specialized areas demanding advanced metallurgy and flawless quality assurance.

Even more impressive are the upcoming prospects. Management, known for its conservatism, anticipates pre-tax profits doubling to over £71 million this year. Supporting this outlook is a record £365 million order book, extending across multiple years from nuclear decommissioning initiatives and the UK’s next-generation nuclear submarines.

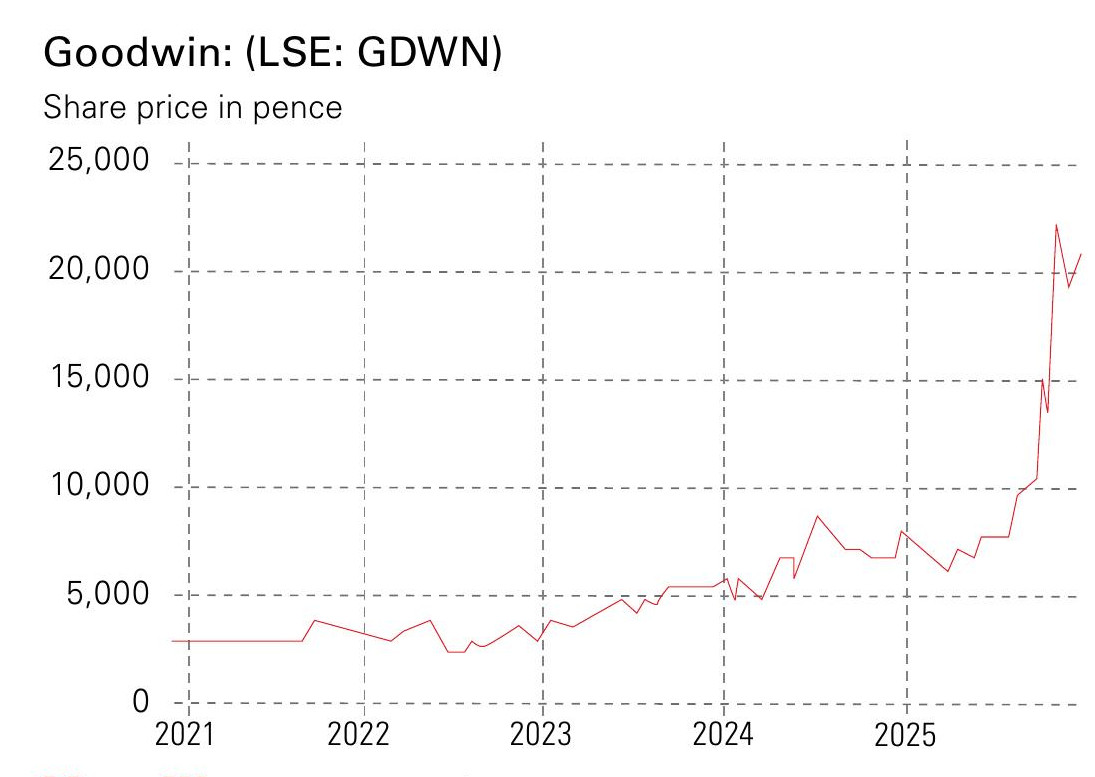

(Image credit: LSE)

Goodwin demonstrates exceptional financial prudence

Unlike typical cyclical industrial firms with average returns, Goodwin has evolved into a high-margin provider of indispensable parts for uncancellable government and corporate programs.

The company’s financial discipline stands out. Rather than borrowing heavily for expansion, it employs a customer-funded investment approach. Major capital projects are linked directly to long-term customer commitments—the customer pledges, and Goodwin invests. This conservative tactic has proven highly effective, boosting cash flow dramatically, eliminating net debt, and prompting a 111% hike in the regular dividend alongside a substantial special payout.

In an industry where peers often depend on heavy debt or share dilutions for growth, Goodwin differentiates itself by expanding while reducing leverage. Investors are drawn to this profile. Moreover, a promising second pillar emerges in Duvelco, its advanced-materials division centered on patented polyimide Ducoya. This material’s properties suit demanding sectors like aerospace, enabling premium margins due to customers’ emphasis on verified performance. Entry barriers include extensive technical approvals and testing, aligning perfectly with Goodwin’s strengths.

Breaking its own protocol, Goodwin funded a new pressing facility for Duvelco entirely from internal cash reserves—a departure from customer-backed investments. Leadership evidently views Ducoya as a potential standalone profit driver. Notably, the projected profit doubling to £71 million excludes any contribution from this subsidiary.

Goodwin justifies its elevated valuation

Promotion to the FTSE 250 has elevated Goodwin’s visibility among index funds and institutional investors, leading to a sharp share re-rating and a premium over conventional industrial peers.

Is this premium excessive? It could be, given the firm’s specialist engineering focus, constrained free float, reliance on major government contracts, and reserved management communication, all contributing to share price volatility. Nevertheless, few UK-listed manufacturers boast a decades-long quality track record, a robust pipeline of state-supported projects, a virtually debt-free balance sheet, expanding margins, and an innovative advanced-materials venture. The higher valuation mirrors these strengths.

The shares carry a premium, but so does the underlying quality. For long-term investors comfortable with moderate liquidity and confident in family stewardship, Goodwin stands as one of London’s premier high-quality industrial growth stories. Existing holders should maintain positions; newcomers should consider purchases on significant dips.